Restructuring China's Auto Industry

Growth stimulated much too much entry

I’m presenting at the January GERPISA conference in Paris. For better and for worse, it’s a virtual conference, or at least my component is. The annual GERPISA conference will however be in person, in Paris June 15-18, 2026. Here are initial thoughts, I’ve drafted a powerpoint so this is a (second) prose draft.

Background

In 2000 China’s auto industry barely existed, a horde of local truck manufacturers, many using a Mitsubishi Fuso derived engine. There were a few low-volume carmakers, First Auto Works and above all the Shanghai Auto Industry Corp - VW joint venture, which made an outdated Santana model using an assembly line imported from South Africa. Then came the SAIC-GM joint venture, with the Buick Sail, a new model. VW quickly replaced their old Santana with the one currently in production in Germany. Prices fell, but a rapidly growing economy created robust demand and SVW and SGM were highly profitable. Other joint ventures followed, many other joint ventures: today there’s passenger vehicle production in 27 of China’s 31 core provinces.

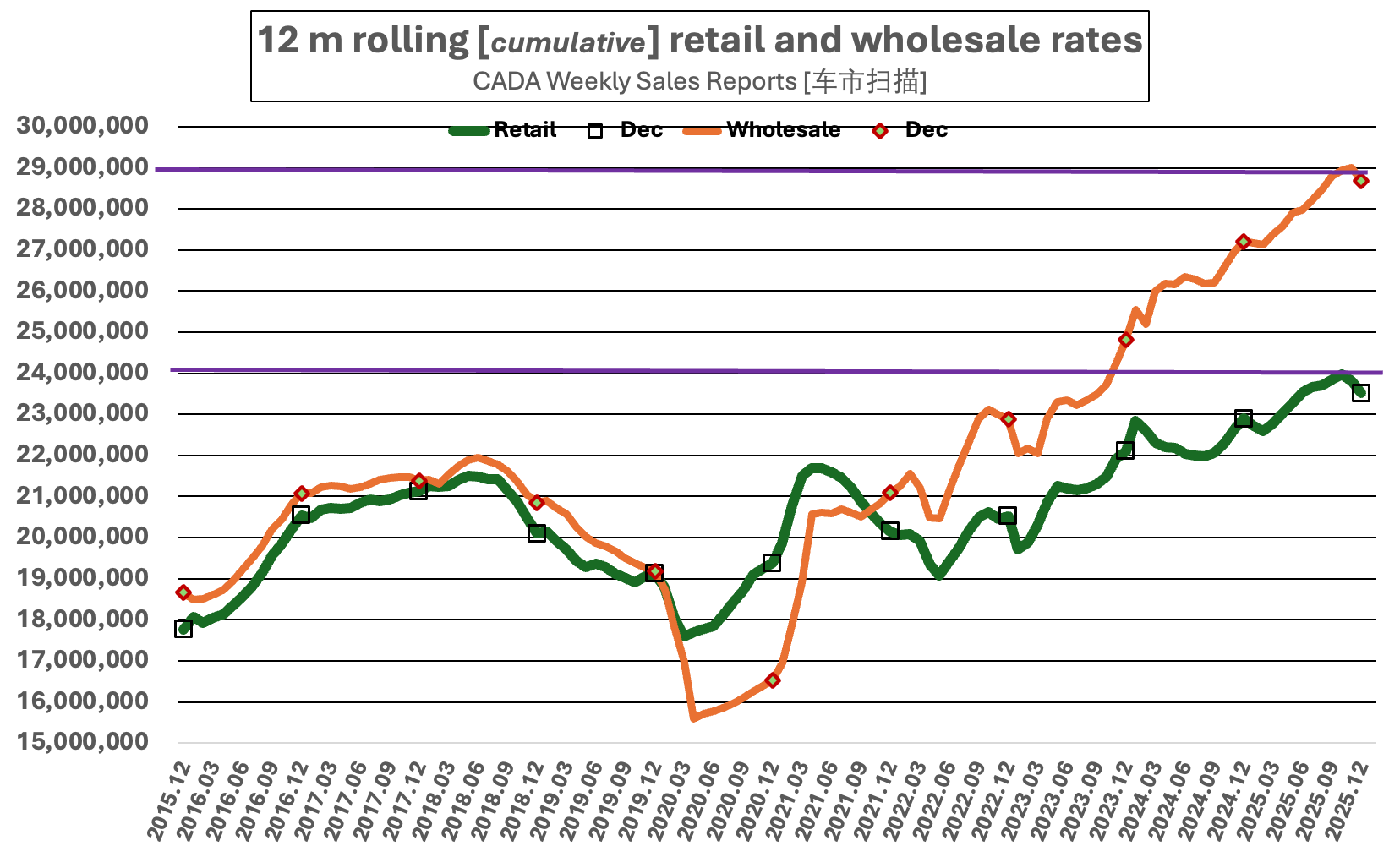

By the end of 2015, sales were running at an 18 million annual rate, surpassing the US and European markets. Ten years later, and (exports included) sales hit 29 million – and that doesn’t include light commercial vehicles.1 For the past decade, that averages to an additional 1 million units of sales every year. Such growth generated new entry, but not everyone has done well – even among joint ventures, Jeep, Suzuki and Mitsubishi Motors have exited the market. There’s excess ICE (internal combustion engine vehicle) capacity.

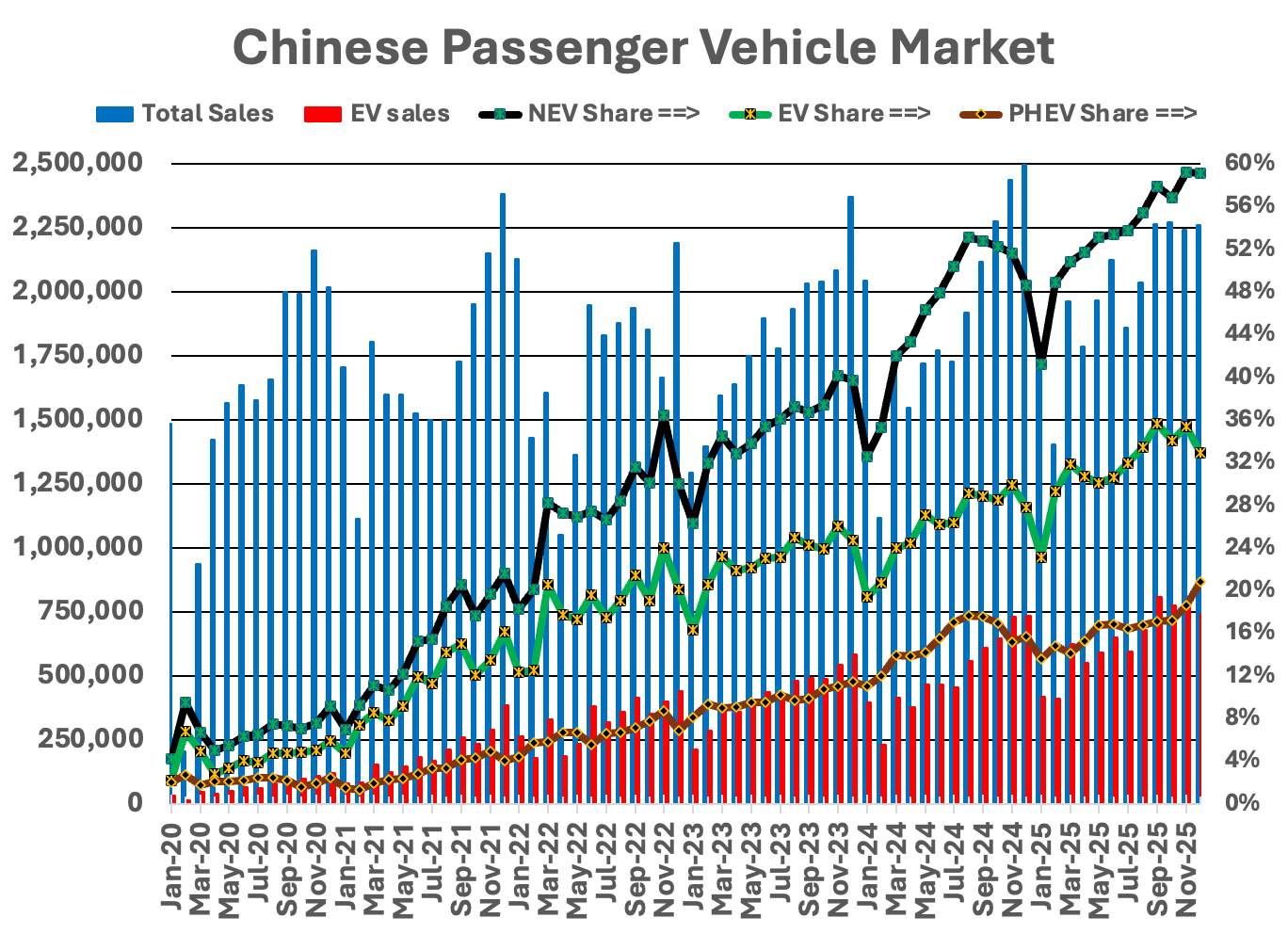

The rise of NEVs (new energy vehicles, EVs and PHEVs) accentuated the excess. In 2020H1 only 404,000 NEVs were sold, and 1,263,000 in all of 2020. Almost none were exported. By 2025 the total was 12,903,000 of domestic sales, plus exports of another 2,423,000 units. That means that in 5 years over 14 million units of NEV capacity was added. The overall market grew, so not all of that represents redundant ICE capacity. Nevertheless, I estimate that the shift to NEVs rendered 2.95 million units of ICE capacity redundant.

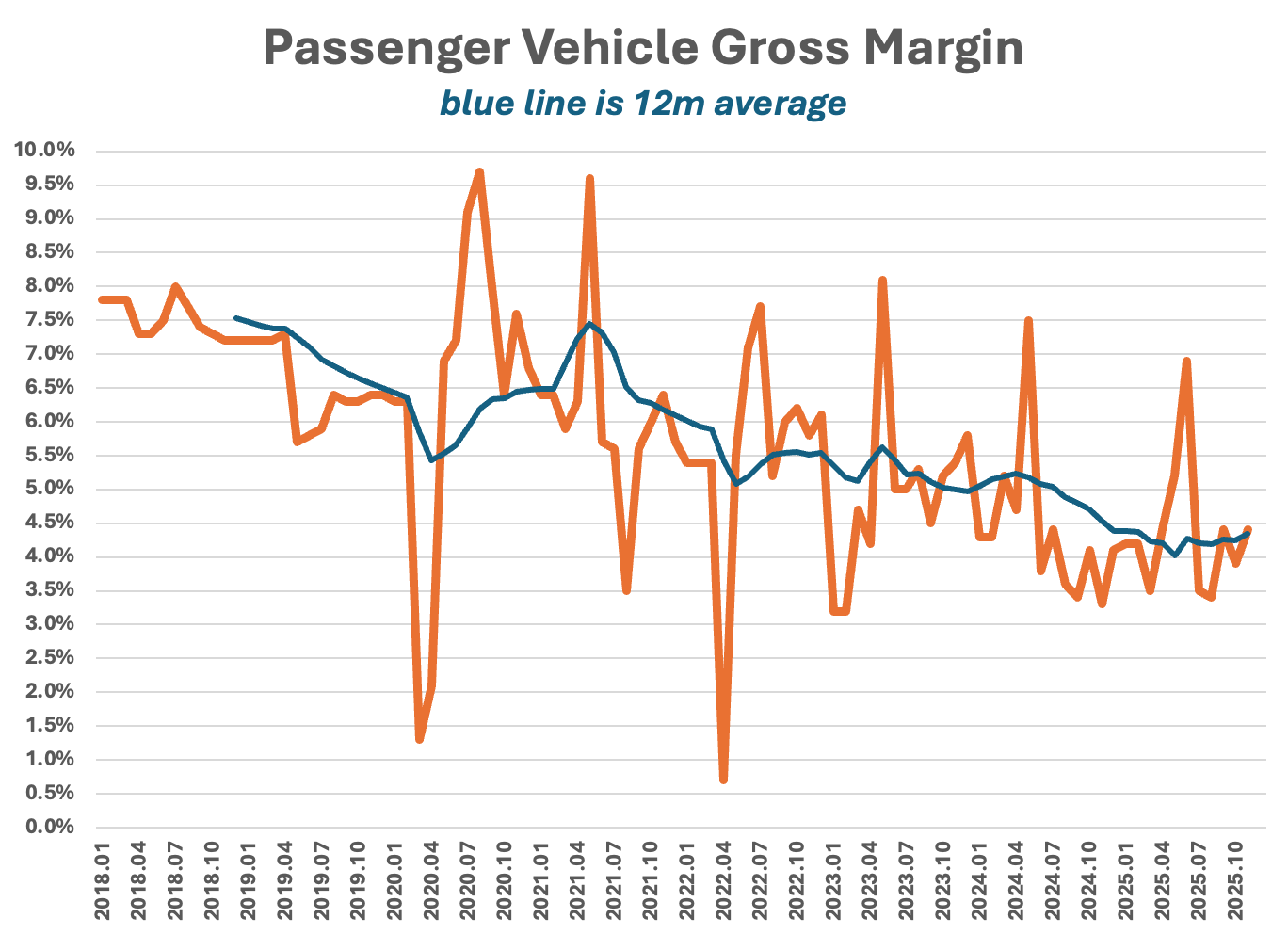

Gasgoo estimates 2024 capacity at 55 million units, and I know of at least another 1 million added in 2025. Since total shipments were under 30 million units, that’s 25 million units of excess capacity. It’s a breathtaking number. Immediate consequences are rampant price reductions, declining profits and surging exports (as firms strive to boost domestic capacity utilization.

Winners and Losers

Losers

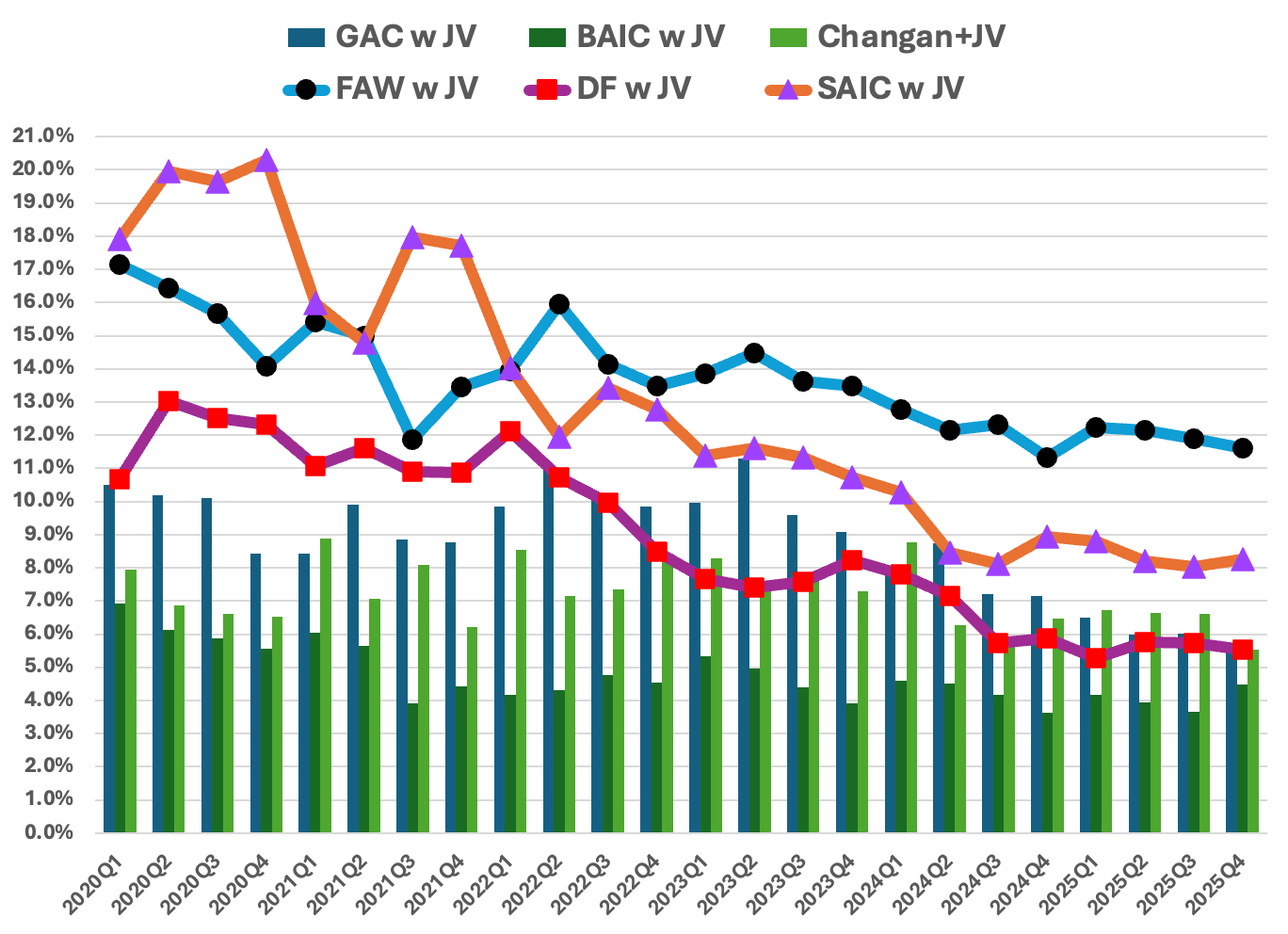

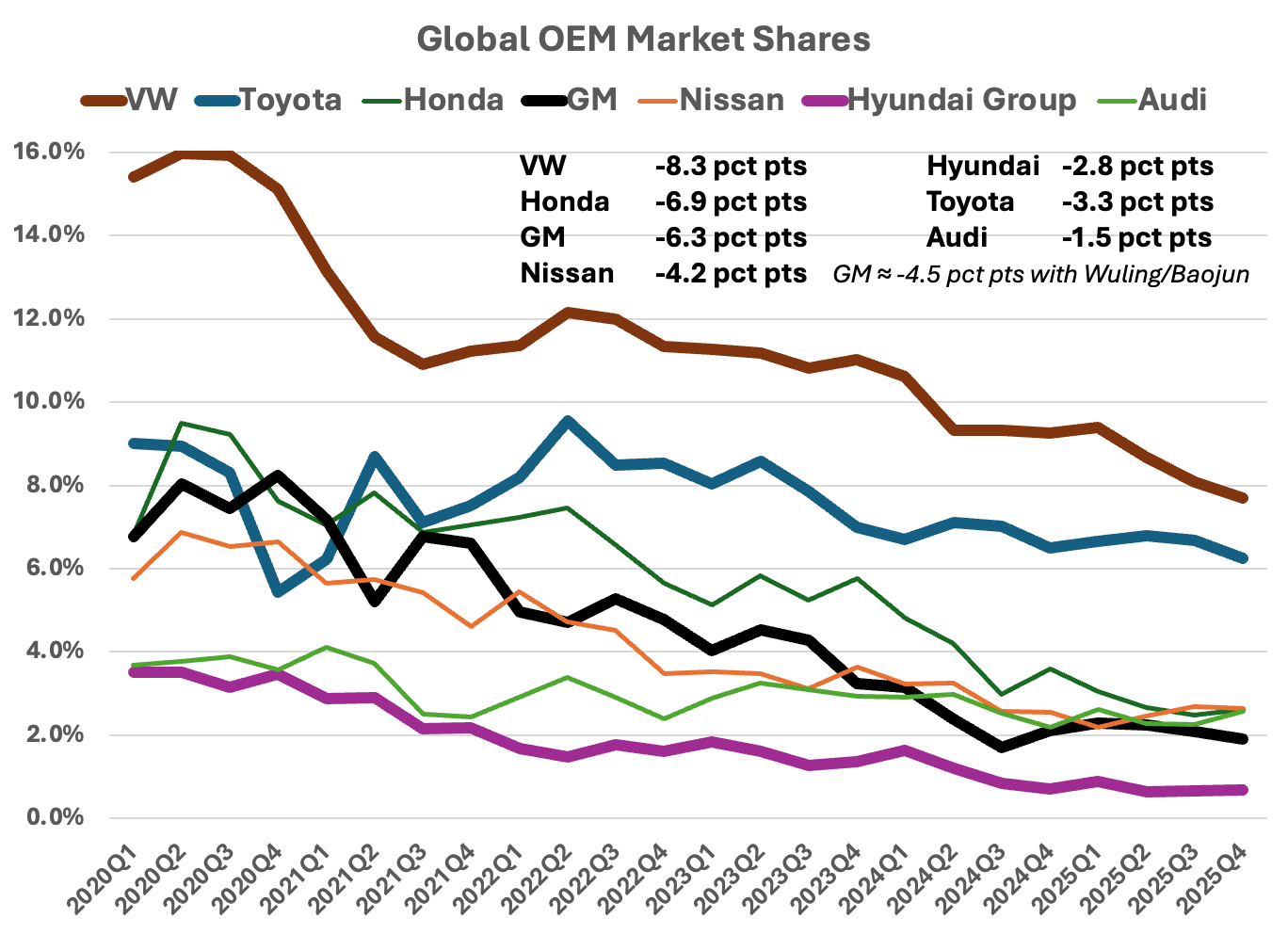

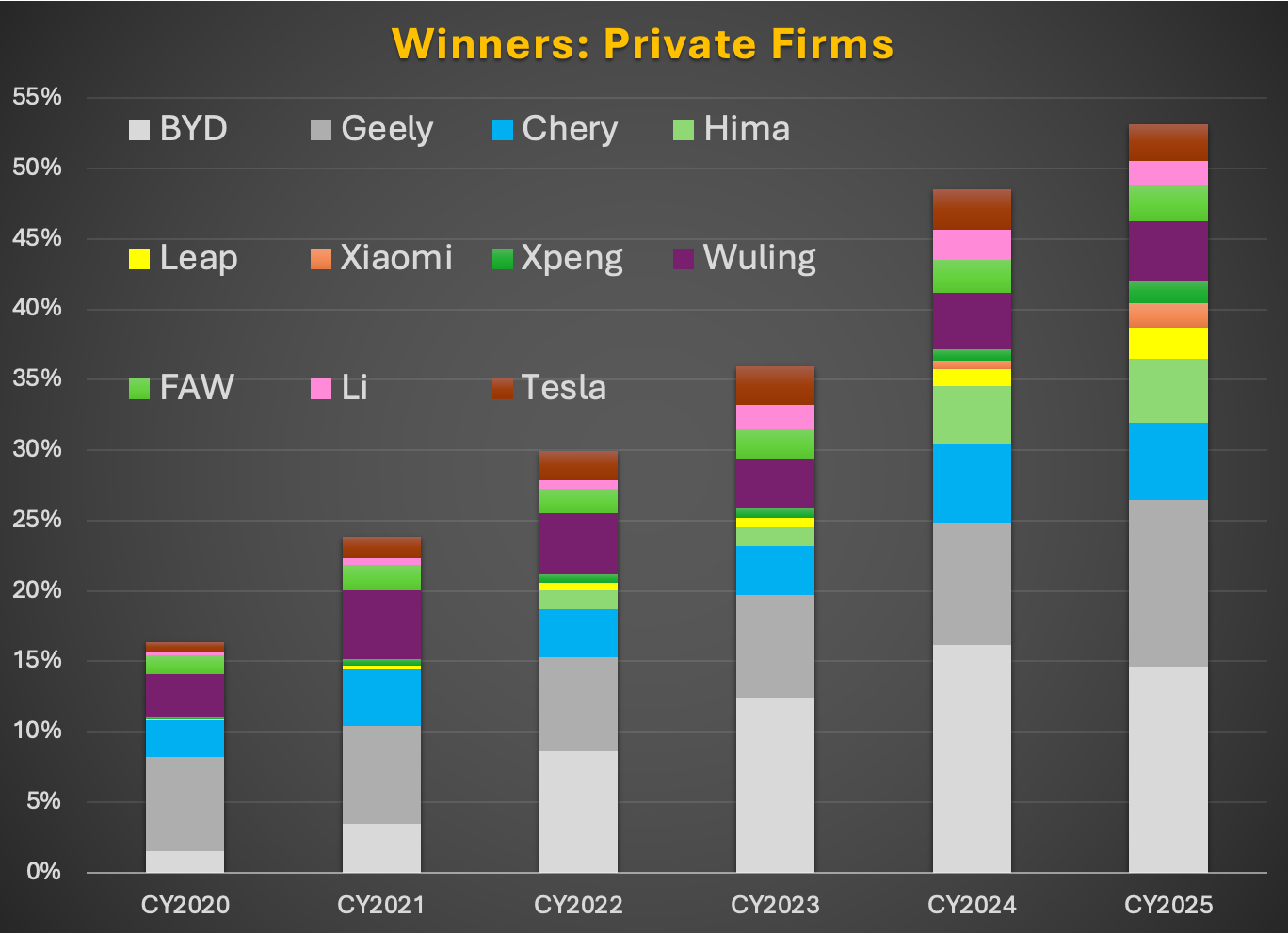

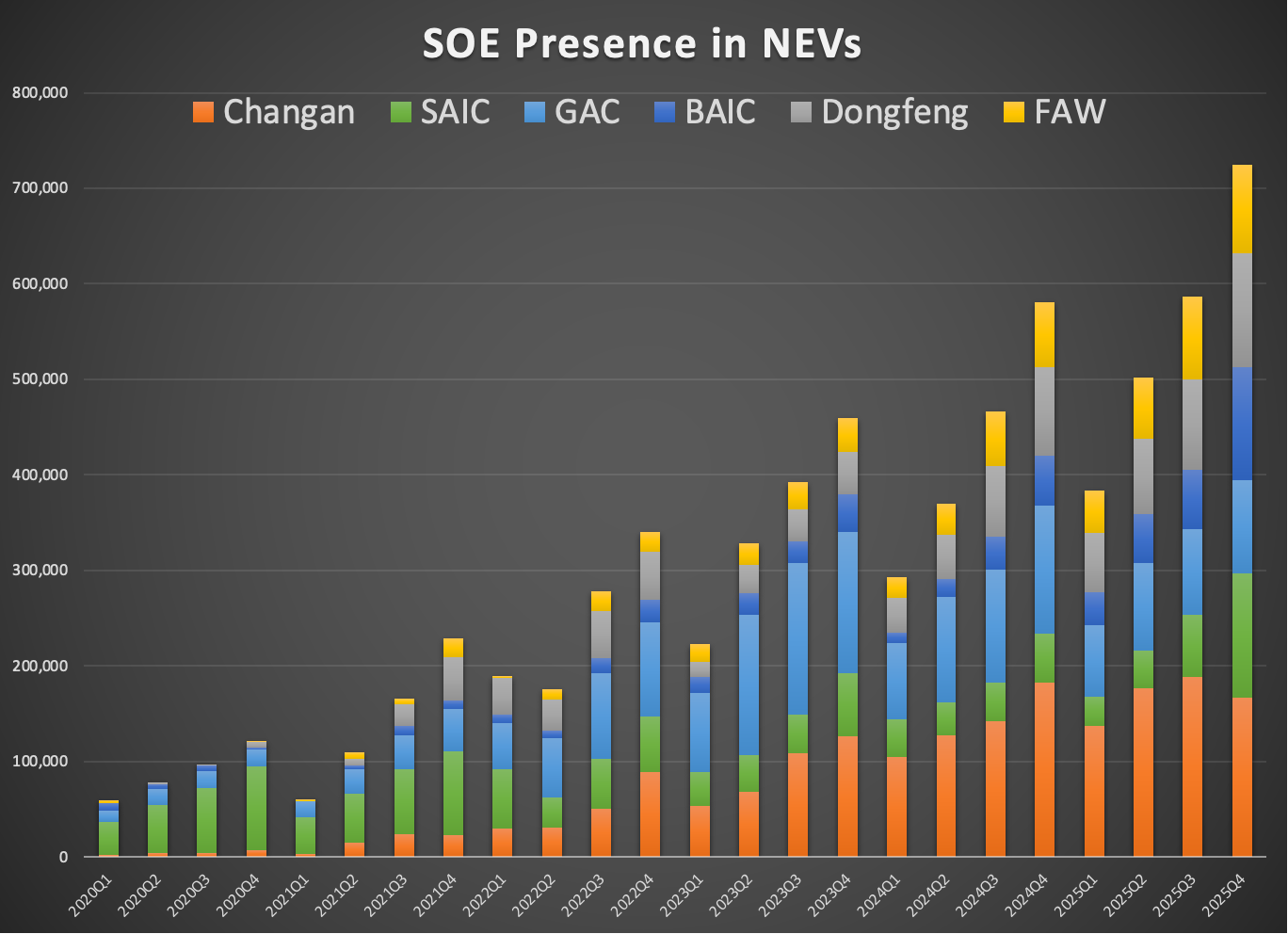

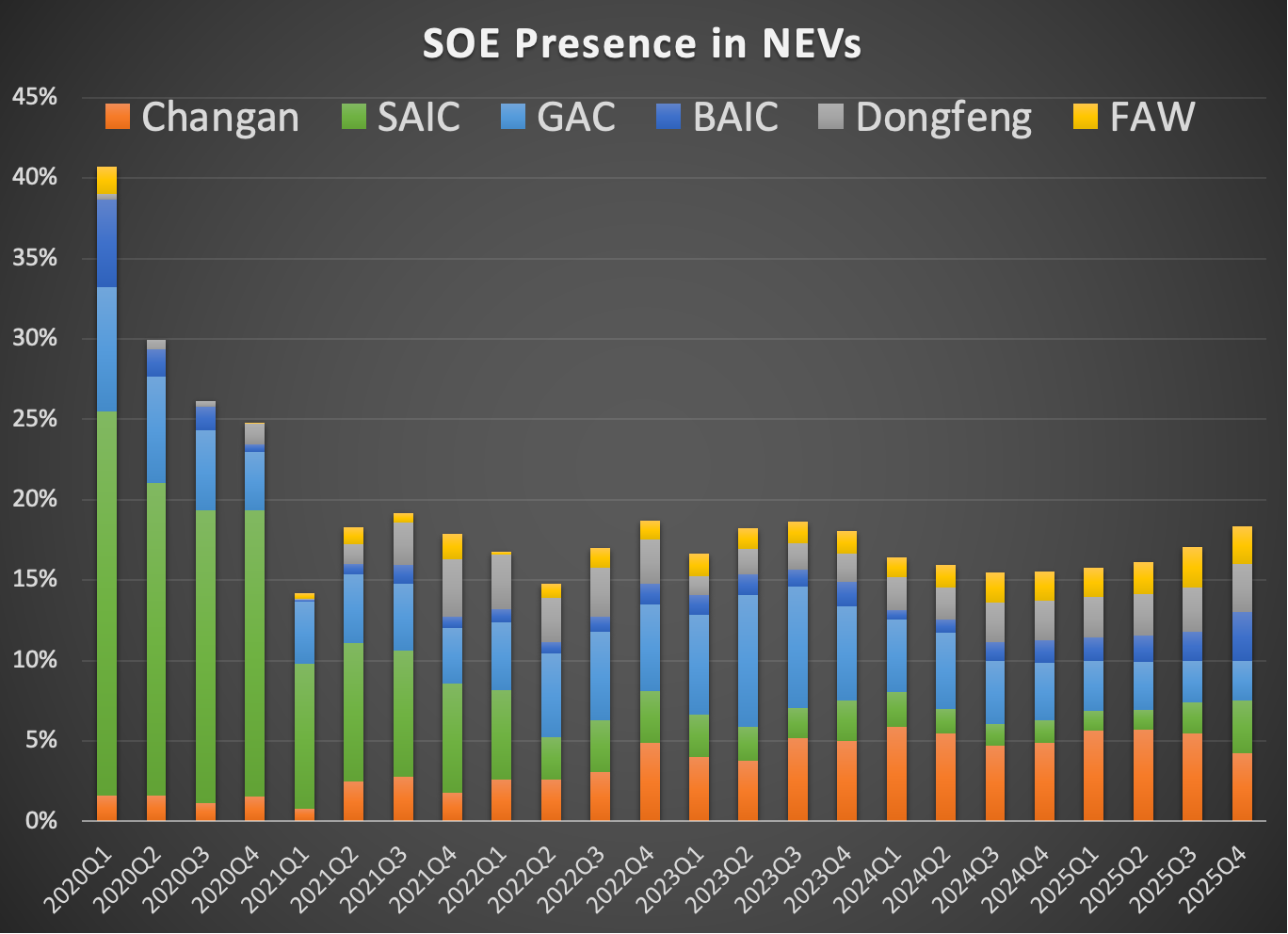

So who has lost out in the transition to NEVs, which hit 59% of the market in December 2025? Above all, it’s the incumbent SOE (state owned enterprises) and their global OEM joint venture partners. In contrast, new entrants – almost all private firms – captured share. Specifically, SAIC and its partners VW and GM are big losers, as is Dongfeng and its partners Nissan and Honda. In general, the SAIC, Dongfeng and the other SOEs leaned on their joint venture partners for profits. While all have their “house” brands, they’ve not done well. So far none have succeeded in the NEV market. The numbers are stark: from peak, VW sales are down 398,000 units and their formerly profitable Audi brand is down 94,000 units, or over 490,000 units. At its recent peak (in early 2020) the VW group had 20% of the entire Chinese market. In 2025Q4 they held 10.3%. SAIC (house brands plus SVW plus SGM) went from 20.3% to 8.3%.

Winners

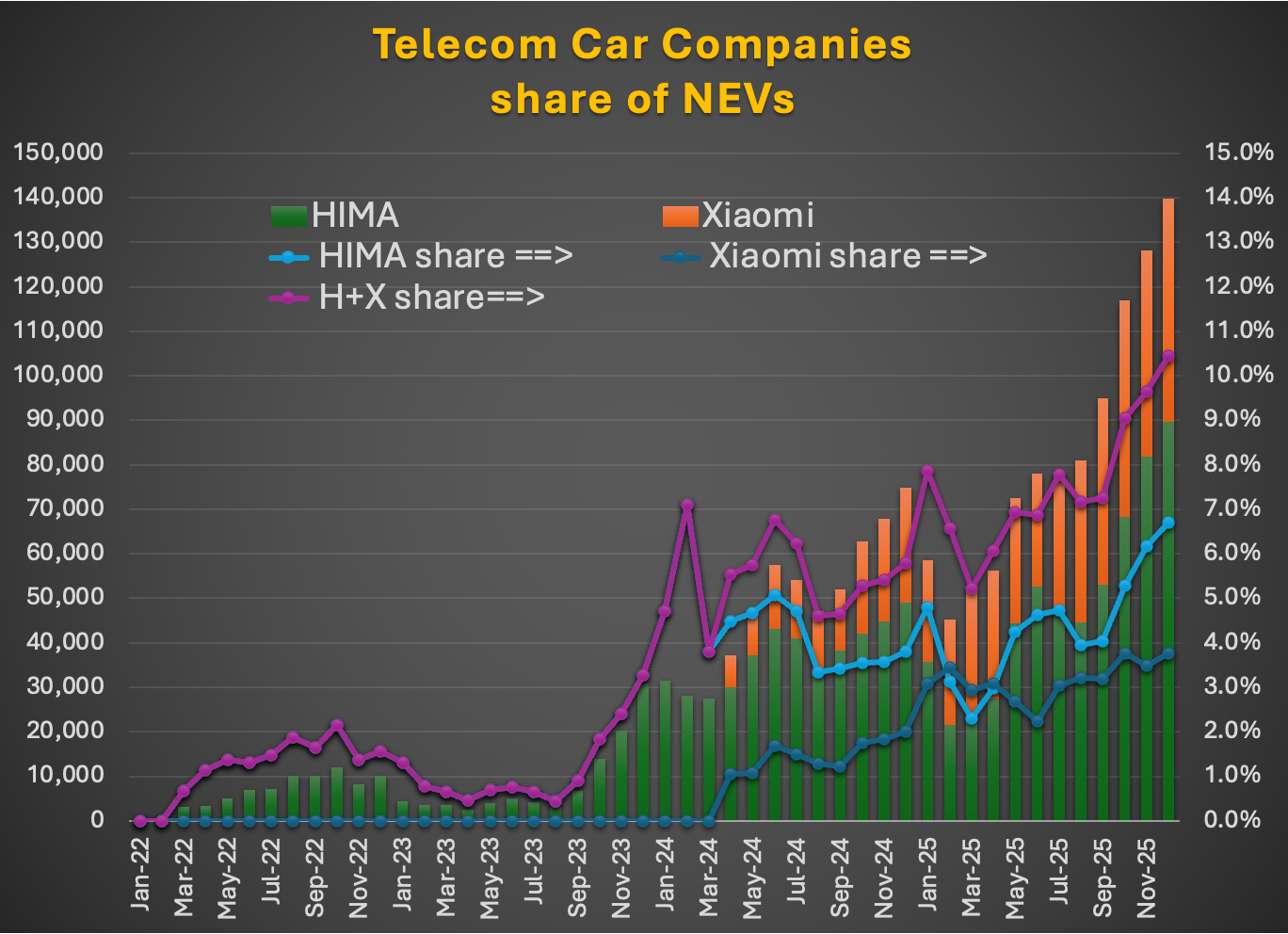

Two firms stand out as winners: BYD and Geely. In January 2020 BYD sold all of 7,600 units. In December 2025 they had 16 different models that sold more than that! Including exports, their December sales topped 420,000, and they are the world’s top EV producer. Geely is older; they began producing cars in the late 2000s, and purchased Volvo from Ford in 2010. They were a third the size of VW in 2020Q1; in 2025Q4 they were 15% larger. But there are others. Two telecoms firms – Xiaomi and Huawei – entered after early 2022; at the end of 2025 they held 10% of the market.

What gives?

Now in a competitive market money-losing firms exit, sooner rather than later. In the auto industry, they tend to hang on. VW has gone through several crises, such as in 1974. The Federal and Lower Saxony governments worked with IG Metal, the dominant union, to finance early retirements and otherwise ease the pain. In the US, Chrysler received a loan package in 1980, while the US Treasury stepped in to provide DIP financing when Chrysler and GM entered Chapter 11 bankruptcy in 2009. Market forces can give way to the political economy of troubled employers who are a huge presence in their local economies and that are highly visible politically. China is no exception.

One example is NIO and the Anhui provincial government. Initially a private firm, NIO has come close to failure twice, only to be bailed out but governmental entities. NIO continues to lose money, and has seen its exports to Europe decline, in contrast to almost every other firm with a presence there. Recently it has increased sales with the launch of low-priced Onvo-brand models, and the initial model of a new Firefly brand. Now low-priced models can’t generate big profits, but by boosting capacity utilization they can help cover fixed costs. That may not work out well, because these new models are being assembled in new plants…

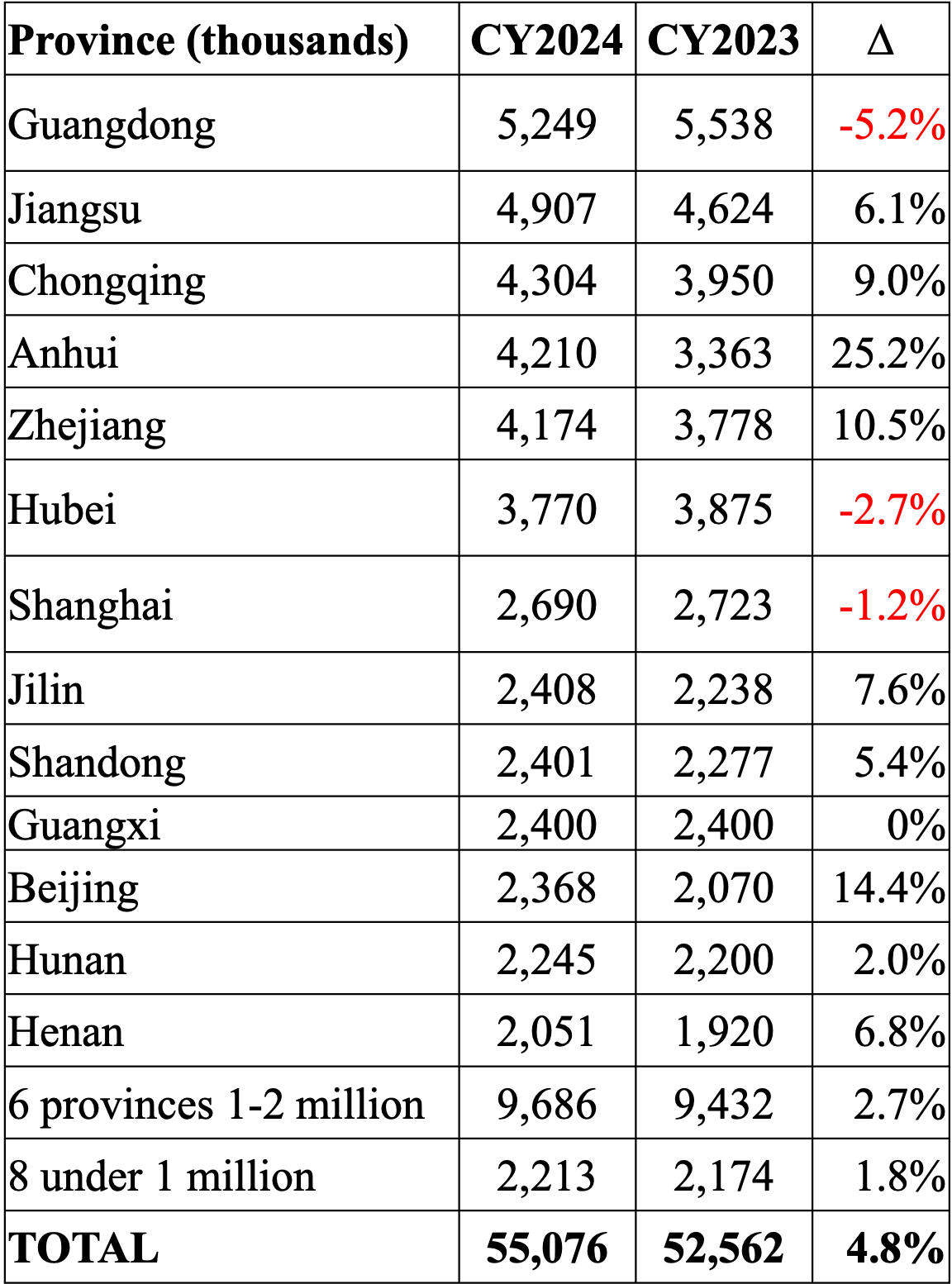

Of course NIO is not alone. Everyone knows how to play the game: VW’s four most recent plants are in four different provinces. Production is widely scattered, as the following table of capacity by province illustrates:

Paths Forward

Growth

China’s population is falling, and 21% are over age 60 so likely past the age at which they’d buy their first car. Another 16% are in their 50s. The largest single cohort is age 35-39, but thereafter each cohort drops in size – the number of 0-4 year-olds is only 40% the number of 35-39 year olds. Growth will be low, and then gradually tail off. For reference, Japan’s passenger vehicle sales peaked in 1997, while it didn’t hit China’s current aging profile until a decade later.

In contrast to post-1990 Japan, where growth has been very low, China’s economy is still expanding,2 and car prices falling. However, real estate remains in free fall, and that affects the wealth of younger generations who poured their income into buying condos, and can’t walk away from their non-recourse mortgages – and construction has halted on millions of those, so they are not salable, even at a loss. Now problems are concentrated in 2nd- and 3rd-tier cities, but that’s where car ownership has room to expand.

That leaves incentives. Until January 1st, 2026 purchasers of ICEs paid a 10% sales tax, purchasers of NEVs 0%. They now pay 5%. While the national new-for-old (以旧换新) scrappage program continues, there are more strings attached and lower caps on payments. So far I’ve not seen discussion of what’s happening to the add-ons provided by many local governments.3 Still, as per the graph above, sales ran at a 20+ million unit rate 2016-18, and those were all ICEs. There are still a lot of 10-year-old cars on the road that predate today’s stricter emissions standards.

Finally, how about further price/cost reductions driving demand? Well, the industry isn’t making money, and the government is trying to dampen the price war among battery producers – battery costs are reportedly rising. Yes, intrinsically less costly sodium-ion batteries are coming along, but it will be the end of the decade before there’s much capacity. Meanwhile, even industry leader BYD is operating below capacity, even though they are now the largest exporter with their own fleet of 8 RO/RO [roll-on, roll-off] ships. And their 2025 price cuts failed to boost demand.4

Exit

There’s been plenty of exit: Aiways, Borgward, Brilliance, CNHD, Dayun, Dorcen, DS, Fujian, Guojin, Hanteng, HiPhi, Hozon, Jeep, Letin, Lifan, Lingtu, Mitsubishi, Qoros, Southeast, Suzuki, Weltmeister, Yantai, Yema, Young, Yujie, Yundu, Yunque, Zedriv, Zotye. Others have minimal sales, Haima, Polestar, Skyworth, SWM. Now Hozon is the parent of Seres, which is doing well as a contract producer for Huawei, while CNHD remains a huge truck maker. In any case none of these were ever major producers. While it’s not clear whether their factories are still counted as part of capacity, in the aggregate they were too small to help, and many exited years ago.

In my view, none of the big players are likely to exit, certainly not the SOEs. The operations of some of the global OEMs are struggling (Ford, Nissan and recently Honda), to the point where I question their viability going forward. However, the larger of the new entrants are doing well enough, and the two most recent – Huawei’s HIMA and Xiaomi – are the growth part of much larger and well-heeled telecoms firms. They’re here to stay, and other firms are still able to raise fresh capital. The exit of a couple smaller firms (such as NIO and Tesla) won’t take enough capacity out of the market, and won’t happen in the next 2 years.

Restructuring

That leaves restructuring. Dongfeng has new management and a new corporate structure. SAIC-VW has (quietly) idled two plants. A bit here, a bit there will trim ICE capacity. (Presumably the same thing is happening at the Tier I’s making pistons, exhaust systems and the like, and not just in China. A decade ago Mahle was a piston maker; today they are a thermal management company.)

What I don’t expect is to see a wave of plant closings. Political economy is at play – the party boss of a province or a Tier I city doesn’t want bad news on their watch.

Entry into NEVs

Worse, the big SOEs are all pouring money into NEVs, launching new brands and (though I can’t document it) part of this is from building new capacity and not just converting existing facilities.5 The absolute growth of the SOE’s “house” NEV sales is impressive. However, they’ve failed to gain market share. See the following two graphs.

Exports

Currently exports are booming, but that will be transitory for two reasons. First, even before 1910 Ford was producing outside the US. For the industry, the rule is “make where you sell.” Cars are expensive to ship, local markets all have their idiosyncracies, and then there’s political pressure. BYD already has plants operating in Uzbekistan, Thailand and Brazil, and plants slated to open this year in Hungary and Indonesia. Geely has plants in Europe and (as Volvo) the US, among other locations. Others are doing the same.

The primary political response, and impetus for building local capacity, are tariffs. Those repress exports from China, but they also fail to repress competition among BYD, SAIC (the MG brand), and all the others. Exports bolster capacity utilization, but require local investment and because of competition among Chinese producers, not unusually profitable.

One policy could change that in favor of Chinese exports: the imposition of VERs (voluntary export restraints) or similar quotas. Why? – those limit intra-Chinese competition. As it happens, I was shopping for a new car when the US negotiated the VER with Japan, which went into effect in May 1981. Between the month between when I started looking and when I actually bought a Toyota Tercel, the price jumped 25%, from $4,000 to $5,000. Furthermore, with the amount any given Japanese firm could export to the US, they had a strong incentive to move upmarket. In Japan, the press started calling Toyota Motors “Toyota Bank.” That proved fortunate, because over the next few years oil prices fell and demand for subcompacts – at peak 42% of the market – collapsed. By that time Toyota and the others had moved to compacts and mid-sized car, using profits generated by the US VER.

Post-publication news flash: Reuters and others report the EU is pushing for minimum prices, on top of tariffs. That’s potentially even better for Chinese firms than a VER, as it lets firms raise prices without limiting volumes.6

Conclusion

I see no short-term path for the Chinese industry out of excess capacity. Instead, I foresee a slow bleeding of money. That’s not good news for the German manufacturers that once dominated the Chinese passenger car market. A black Audi used to be the car of choice for mid-level Communist Party officials. Taxi companies and then individual owners bought Santanas. BMW and Mercedes held the luxury end, and then there were all those imported Porsches.

Instead, BMW started off 2026 by cutting prices for 31 models, most of about 10%.7 So I may be wrong in my analysis: for the rest of the decade, firms may hemorrhage, not bleed, money.

Pickups are one such, they’re work vehicles in China. Total output Jan-Nov 2025 came to only 537,000 units, less than Ford F-150 sales in the US. Domestic sales were much less, because 52% of output was exported. In cities, vans and box trucks are more common; I did not see a single pickup truck in Shanghai during my June 2025 visit, and only one in Hangzhou.

All numbers are from my database of model-level domestic sales, which starts in January 2020 and now covers 1,150 models, with 670 models reporting positive sales in December 2025. For all these models I have drivetrain, segment, price range, brand, manufacturere (including joint venture partner) and monthly sales. I have supplemental data on monthly exports, used vehicle sales and commercial vehicle sales, and weely aggregate sales going back to January 2015. As of January 11th I still lack December data for a half dozen or so models, which will affect my totals by only a few thousand units.

Porsches are not assembled in China. It used to be their largest market, with China importing over 94,000 units in 2022. In 2025 the total will likely be less than half that. Adding their loss puts the VW group down over 500,000 units.

Huawei’s strategy is unique: they contract all their production to other firms under the HIMA umbrella. Almost the entire output of Seres (the Aito brand) is devoted to HIMA vehicles, but Huawei also has contracts with several SOEs, all of whom have excess capacity.

See Nick Lardy’s December 2025 PIIE article for growth prospects. Nick was a visiting scholar at Yale while I was a grad student. Look as well for anything by Barry Naughton (UCSD), a fellow grad student, and by Loren Brandt.

Provincial and municipal governments face tighter budget constraints. However, as I read the details, some of them didn’t actually require scrapping, but my guess is that most of those who received local subsidies applied for the national program, which does require scrapping.

For more on BYD see my November 2025 SeekingAlpha article, “Q3 2025 China Update: At BYD, Domestic Problems Dominate,” which is however behind a paywall.

SOEs have privileged access to funding, and soft budget constraints.

An initial challenge with the US negotiating the VER with Japan was that it divvied up the market on the basis of market shares. That proved unacceptable, as at that time GM held a controlling stake in Isuzu, which was tooling a plant to make vehicles for export to the US market. The problem was that their export share was minimal, and accepting a VER with no GM allocation would have rendered that investment a big financial waste. I expect the EU will face similar challenges in fixing the details.

打响2026价格战第一枪!宝马31款车型官降最高降30.1万元!, January 4, 2026 at 车主之家. You can run the link through Google Translate, which does a pretty good job on this sort of material.

GERPISA conference Zoom link

Time: Jan 15, 2026 02:00 PM Paris-Brussels

Tommaso Pardi: From Eldorado to existential threat: the changing role of China

and the return of protectionism

Mike Smitka: Restructuring China's Auto Industry. Growth stimulated much

too much entry

Martin Schroeder: The expansion of Chinese OEMs to Southeast Asian

markets

John Paul MacDuffie: Strengths and weaknesses of Chinese OEMs amid the price war and

overcapacity crisis

https://cnrs.zoom.us/j/97102954238?pwd=nz4rbqX2o4ne1efbQ0WJKvvxI8eRH2.1

Meeting ID: 971 0295 4238

Passcode: i9JuJ9

Mike, this is the "Gladiator School" syllabus.

You see "Excess Capacity" and "Bleeding." In the ChinArb framework, System B sees "Evolutionary Pressure."

1. The "Spartan" Selection Process Beijing knows it doesn't need 100 car companies. It needs 3 global killers. The 25 million units of excess capacity is the Furnace. The fact that SOEs and JVs (VW/GM) are the ones bleeding suggests the policy is working as intended. The state is letting the "Zombies" starve to feed the "Apex Predators" (BYD, Huawei). This is not a market failure; it is a controlled burn of the legacy forest to let the new species grow.

2. The EU "Minimum Price" Trap (Toyota Bank 2.0) Your analogy to the 1981 Japan VER is brilliant. If Brussels sets a Minimum Price, they are effectively banning Chinese firms from discounting.

Result: You force BYD to raise prices (guaranteeing them fat margins) and force them to move upmarket (adding tech/luxury to justify the price).

Historical Rhyme: The US trade restrictions turned Toyota into Lexus. The EU trade restrictions will turn BYD into a premium tech brand. System A is about to force System B to become more profitable.

3. The "New Species" Invasion The most terrifying chart is the rise of the "Telecom Car Companies" (Huawei/Xiaomi). This is Asymmetric Warfare. While Detroit tries to figure out batteries, Huawei is integrating the car into the Operating System of Life. They aren't selling transportation; they are selling a Mobile Node. The "Restructuring" you describe isn't just about factories closing; it's about the definition of the automobile being rewritten.